As of January 1, 2026, Indonesia has fully transitioned to the Coretax system. This modernization has standardized tax identification for all entities and individuals, including those residing outside the country.

-

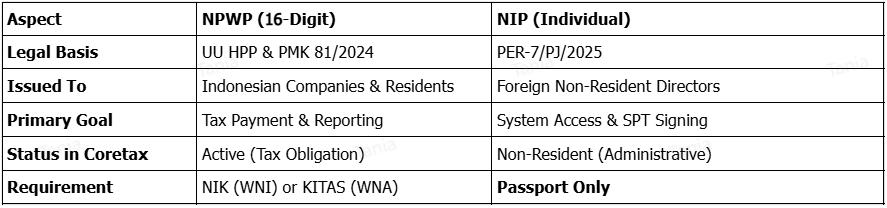

The 16-Digit NPWP (Corporate Tax ID)

Every legal entity in Indonesia is now required to use a 16-digit NPWP.

-

The Change: The old 15-digit format is retired. Existing companies have had their numbers converted by adding a “0” at the beginning or receiving a new 16-digit sequence.

-

Regulation: PMK No. 112/PMK.03/2022 (and its amendments) and PER-6/PJ/2024, which mandate the 16-digit format for all taxpayers (Individual, Corporate, and Government).

-

NIP for Foreign Directors: The Digital Identity

For foreign directors who do not reside in Indonesia (Non-Residents), the Nomor Identitas Perpajakan (NIP) serves as their unique digital identifier within the Coretax portal.

-

Function: It is not a tax-paying ID for the individual, but an administrative “key” that allows them to log into the corporate account and legally sign Electronic Tax Returns (SPT).

-

Regulation: PER-7/PJ/2025 regarding the technical procedures for registration and identification in the Core Tax Administration System.

-

Key Clarification: NIP vs. KITAS

It is a common error to assume a director needs a residency permit (KITAS) to be registered in the tax system.

-

Fact: A foreign director can obtain a NIP using only a valid Passport.

-

Resident vs. Non-Resident: * If the director lives abroad: They apply for a NIP (Non-Resident status).

-

If the director lives in Indonesia (>183 days): they must obtain a KITAS and a 16-digit NPWP (Resident status).

-

-

Regulation: PER-7/PJ/2025 specifies that for Non-Resident Individuals (Subjek Pajak Luar Negeri), the required document is a copy of a Passport and a “selfie” with the passport for digital verification.

-

Comparison: NIP vs. NPWP (Summary Table)

-

Why This Matters in 2026

Under the Coretax system, the “signer” of a tax return is no longer just a name on a PDF. The system requires a Validated Digital Identity.

-

Electronic Signing: A director cannot sign the Corporate SPT unless their NIP is registered and linked to the company’s profile in Coretax.

-

Legal Liability: The NIP ensures a clear audit trail. PMK 81/2024 emphasizes that the “Person in Charge” (PIC) must be clearly identified through these digital IDs to ensure accountability.

-

Automatic Integration: The system is now linked with Immigration (Dirjen Imigrasi). If a NIP holder stays in Indonesia longer than the permitted “non-resident” threshold, the system will automatically flag them for a status change.

-

Registration Procedure

The registration is now entirely digital through the Coretax Portal:

-

Account Creation: Foreign director registers as a “Non-Resident Individual.”

-

Identity Verification: Uploads passport and completes biometric verification (PORO – Proof of Record Ownership).

-

Linking: The company’s “Primary PIC” (usually a local director) adds the foreign director as an “Authorized User” or “Signer” within the corporate dashboard.

Legal Disclaimer: This guide is based on PER-7/PJ/2025 and PMK 81/2024. While NIP registration does not require a KITAS, any director performing operational work inside Indonesia still requires a work permit (RPTKA) and stay permit (KITAS) under Manpower and Immigration laws.